The conventional long-term buy-and-hold investment strategy is a little simpler than most but can be just as effective. It's perhaps the most common way to invest in real estate, outside of your primary residence. It works by purchasing a property you intend to keep for a considerable amount of time—anywhere between five and thirty years or more. Most commonly, these are single and multi-family or apartment complexes.

Historically, the value of real estate has consistently risen over time. So, investors know over time, the value of the property will continue to increase, and all they need to worry about is continuing to make their monthly payments. In addition, depending on interest rates, investors typically lock in a fixed loan with long-term rentals, meaning their principal and interest (P&I) payments will never increase. Knowing that, it's important to look for properties in areas with good price-to-rent ratios and potential for growth.

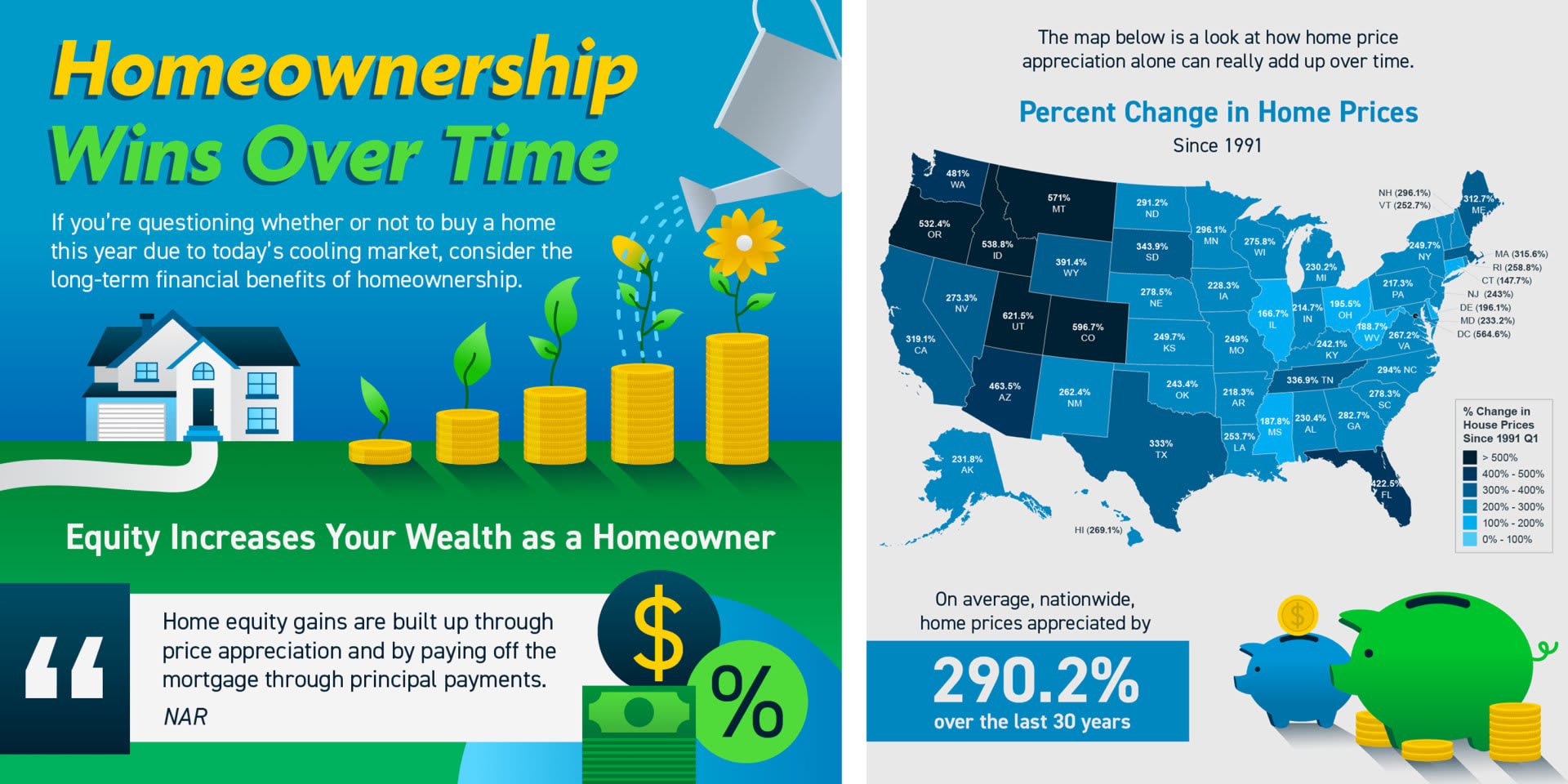

To take on the least amount of risk and maximize your investment, you need to purchase a property where the rental income exceeds P&I payments, property taxes, home insurance, management fees (if applicable), and all other expenses. This means you'll be collecting consistent cash flow each month, which can range from a couple of hundred dollars to a couple of thousand dollars depending on the rental income of the property you purchased. In addition, the rental income your tenants pay will also increase the equity you own in the property as your loan is paid off more and more each month. Then, once the loan is fully paid off, investors might sell their property for a profit, as it'll historically always be worth more than what they bought it for if enough time has passed. On average, nationwide, home prices appreciated 290% over the last 30 years. In Washington State, home prices have appreciated around 481% since 1991. Even with the dramatic increase in value over time, once the loan is paid off, renting the property is still a popular choice among investors. All the rental income will now be passive cash flow, as you won't have monthly P&I payments anymore.

After purchasing the property, you can hire a property manager/management company that charges a percentage of your rental income, typically between 8-11%. They can deal with the tenants, marketing, accounting, maintenance, and most other responsibilities of being a "landlord." That way, you won't have to worry about getting woken up by a tenant's call in the middle of the night. Of course, you can also take on landlord responsibilities moving forward and manage it yourself; if this is the case, it's important to research property management, so you know what to expect and how to handle certain situations.

The catch, or difficulty, with typical long-term buy-and-hold investment rental properties is that the required downpayment is typically between 20-25%. Although the return on your investment can be excellent, the problem can be saving enough money for a downpayment to get started and buy your first property. However, there are plenty of ways to purchase investment properties without paying a 20% downpayment. The most similar investing strategy that allows a downpayment of around 3.5% is called "House Hacking," which you can read more about on my website under "Investing Strategies".